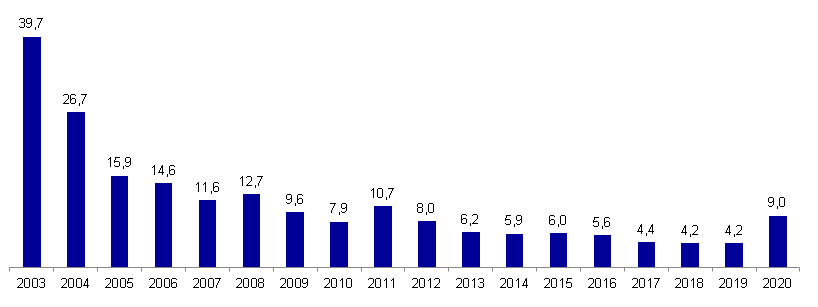

Trading costs are made up of two components: The direct or explicit trading costs of a transaction, which arise from the settlement of the order by banks and exchanges - these include fees and commissions charged directly to investors. And the indirect or implicit trading costs of a transaction, which result from the spread, i.e. the bid-ask spread, and the underlying trading volume. The latter are only comprehensible to a limited extent, as they depend on the composition of the order book and are not shown directly. Nevertheless, they are usually even more important for investors: they can fluctuate by up to 30 percent